Ready to jump into the fix and flip market? Explore this list to find out where you have the best chances of turning a profit.

In 1987/1988 Warren Buffett placed nearly 25% of Berkshire Hathaway’s net worth into Coca-Cola stock. Since then, value investors have wondered what Buffett saw in the stock and how he had the confidence to place such a large portion of his portfolio into one stock. I’ve been able to obtain several of Coke’s shareholder letters from the 1980’s and have been evaluating the numbers myself. The 1988 report in particular shows a company with a clear plan in place to take over the world. Back then Coca-Cola still had plenty of opportunity to benefit from a “Lollapalooza effect” of 1) increasing customer base, as Coke expanded into more world markets, and 2) increasing consumption by existing customers, as sodas became a greater part of the american and developed worlds’ diet.

The 1988 Letter is both a celebration of the turnaround success led by CEO Robert Goizueta, and a realization that billions of people at the time had yet to have their first coke.

Investor Mohnish Pabrai has described several things Buffett might’ve been looking at:

- He found that, like a software company, their gross margin on their syrup sold to bottlers is well over 80%. Coke’s future success was a function of the number of servings of coke sold worldwide. The more the servings, the more the cash flow. He found that over the last 80 years, their syrup volumes sold had risen every single year. The last 80 years included many ugly world events – World War I, the great depression, World War II, The Korean War, The Vietnam War, The Cold War, numerous recessions, being kicked out of India in the 1970s et cetera. Through all of that, Coke has grown every single year. The question Munger and Buffett posed to each other was simple – What volume of syrup might The Coca-Cola Company conservatively be expected to ship in the year 2000…2025…2050? They probably came up with some mouth-watering numbers, then extrapolated free cash flow (about one cent per eight-ounce serving) and finally arrived at a present value of all that future cash flow.

- In 1886, when Coke was first concocted, it sold for five cents per eight-ounce serving. Today, one can buy eight ounces of Coke on sale for under 17 cents. If Coke’s pricing had moved in lockstep with inflation, we’d be paying several dollars for a single can. This is a very unusual product whose unit price has declined dramatically over the years. Very few consumer products have demonstrated the level of decline in prices that Coke has over the last century.

- Billions of people around the world have yet to have their first Coke. In addition, the daily per capita consumption of bottled beverages around the world is miniscule compared to that of the United States and Europe. However, it has risen dramatically in various countries as per capita incomes have risen. We are likely to see big increases in per capita incomes in the third world over the coming decades.

The typical hammer-wielding Wall Street analyst is fixated on the next few quarters, not the next half century when trying to figure out any given company. No Wall Street analyst’s mental model of Coke in 1988 was comprised of the latticework that Munger and Buffett fixated upon. Individual investors will do well if they only made investments within their circle of competence based on an independent latticework of mental models. When all your mental models all converge at about the same intrinsic value for a given business, and that value is well above the price of the business, back up the truck.

Well enough introduction, read for yourself what Warren Buffett was reading in 1988:

A monthly S&P 500 closing price which is higher than the close 4 months prior is a measure of market momentum made popular by Tom Demark. The markets often swing in approximate 9 month moves. An uptrend lasting 34 months has only happened twice since 1950. Until June of this year, The S&P 500 went 34 consecutive months with each monthly close higher than that 4 months prior. The last time the S&P 500 went this long (exactly 34 months ending July of 1956), it subsequently fell 20% over the following year. These two episodes are the longest such streaks since 1950.

Here’s a picture of this historic market momentum, now broken:

This historic momentum was discussed in: Stock Market Uptrend is the Most Overbought in 40 Years.

The S&P 500 recovered in July to record a new tick in the positive direction, however the overall back of the market’s momentum has been broken. (a 1-month false recovery also happened in 1956 before the market fell hard.)

These signals can be followed with my Trend Exhaustion Stock Market Timing Excel Spreadsheet.

I’ve been moving to cash over the last year, so am looking forward to picking up some stock market bargains if the opportunity presents itself.

Via Damn Right: Behind the Scenes with Berkshire Hathaway Billionaire Charlie Munger:

It is 1884 in Atlanta. You are brought, along with twenty others like you, before a rich and eccentric Atlanta citizen named Glotz. Both you and Glotz share two characteristics: first, you routinely use in problem solving the five helpful notions, and, second, you know all the elementary ideas in all the basic college courses, as taught in 1996. However, all discoverers and all examples demonstrating these elementary ideas come from dates transposed back before 1884. Neither you nor Glotz knows anything about anything that has happened after 1884.

Glotz offers to invest $2 million, yet take only half the equity, for a Glotz charitable foundation, in a new corporation organized to go into the non-alcoholic beverage business and remain in that business only, forever. Glotz wants to use a name that has somehow charmed him: Coca-Cola.

The other half of the new corporation’s equity will go to the man who most plausibly demonstrates that his business plan will cause Glotz’s foundation to be worth a trillion dollars 150 years later, in the money of that later time, 2034, despite paying out a large part of its earnings each year as a dividend. This will make the whole new corporation worth $2 trillion, even after paying out many billions of dollars in dividends.

You have fifteen minutes to make your pitch. What do you say to Glotz?

Flipping houses is NOT like on TV — and you’ll likely run into a host of issues as a beginner. Learn from an expert with these 11 extremely helpful tips!

Source: Flipping Houses: 11 Expert Tips for Success, Beginning to End

Consider these amenities when researching homes you might purchase for yourself or as rental income properties:

Most people prefer modest, modern homes.

Most people prefer modest, modern homes.

Source: 3 features Americans want in their dream home – MarketWatch

U.S. homeownership dropped to a record low in the second quarter as more Americans opted to rent, data showed Tuesday. The number of occupied housing units grew, but all on the renter side. The number of owner-occupied units fell from a year ago. No wonder both rents and occupancies continue to soar.

More Americans are renting than ever before. That means this is the greatest opportunity in our lifetimes to own rental property. Earn consistent passive income while the value grows through property price appreciation. If you’re interested in analyzing properties for potential purchase, take a look at my Rental Income Property Analysis for Excel Spreadsheet.

The Rental Income spreadsheet analyzes 10 years of cash flows and gives your true return on investment.

Source: Homeownership rate drops to 63.4%, lowest since 1967

I’m proud to release the Fix-N-Flip Rehab Program For Excel. This Excel calculation tool provides a comprehensive look at the buying, holding, selling and repair costs in order to determine the Maximum Purchase Price you should offer on rehab real estate projects. You can Fix and Flip real estate for great profits if you enjoy doing the research to analyze good candidate properties. Use the program to analyze your profits and minimize risks! The Program includes the popular “70% Rule” for house flipping. The accompanying article contains a short video tutorial and screenshots.

Full Article: Fix-N-Flip Rehab Program For Excel

The Fix-N-Flip Program is available from the Research Offers Page.

Warren Buffett in his 1998 Letter to Shareholders:

When we consider investing in an option-issuing company, we make an appropriate downward adjustment to reported earnings, simply subtracting an amount equal to what the company could have realized by publicly selling options of like quantity and structure. Similarly, if we contemplate an acquisition, we include in our evaluation the cost of replacing any option plan. Then, if we make a deal, we promptly take that cost out of hiding.

Paying employees with stock options is an expense that affects the intrinsic value of a firm. Be sure you are fully accounting for them. Thankfully in 2004, the Financial Accounting Standards Board (FASB) mandated that the cost of options be reflected in the Income Statement, not buried in the footnotes. Investor’s however must still be on guard:

1) Unfortunately almost every company still reports their quarterly earnings to the media as excluding the cost of stock-based compensation. These non-GAAP earnings do not follow the FASB principles. Do not base your P/E multiples off those earnings. See this Fortune article for a description of the problem. This means investors must analyze the Income statement to determine true economic earnings.

2) Use Diluted Shares Outstanding – these account for current in-the-money stock-based compensation (and convertible preferreds) that are outstanding and not yet exercised.

3) Finally, refer to the Notes to Financial Statements to see the Fair Value of remaining unexercised options and other share-based plans (ie. Restricted Stock Units – RSU’s). Reduce your intrinsic value estimate of the firm by this amount. Search for the term “unrecognized compensation cost” within the 10-k or annual report to locate. Add up all values for remaining stock options, RSU’s, etc. For example, Google has $9.7 Billion (about $14 per share) of “unrecognized compensation”, which are future earnings that will go to employees rather than shareholders.

For some companies this is a gigantic expense. From the Fortune article:

over the past two decades, Adobe has spent almost $11 billion repurchasing shares, mainly to offset the dilution resulting from the exercise of employee stock options. Despite all the cash that has gone out the door, the share count is not much lower than it was 20 years ago. If you consider that cash as an expense of running the business (offset by the proceeds and the tax benefits from the stock issuance) then Adobe’s free cash flow over the last two decades is not a robust $9.3 billion, but rather a meager $2.3 billion.

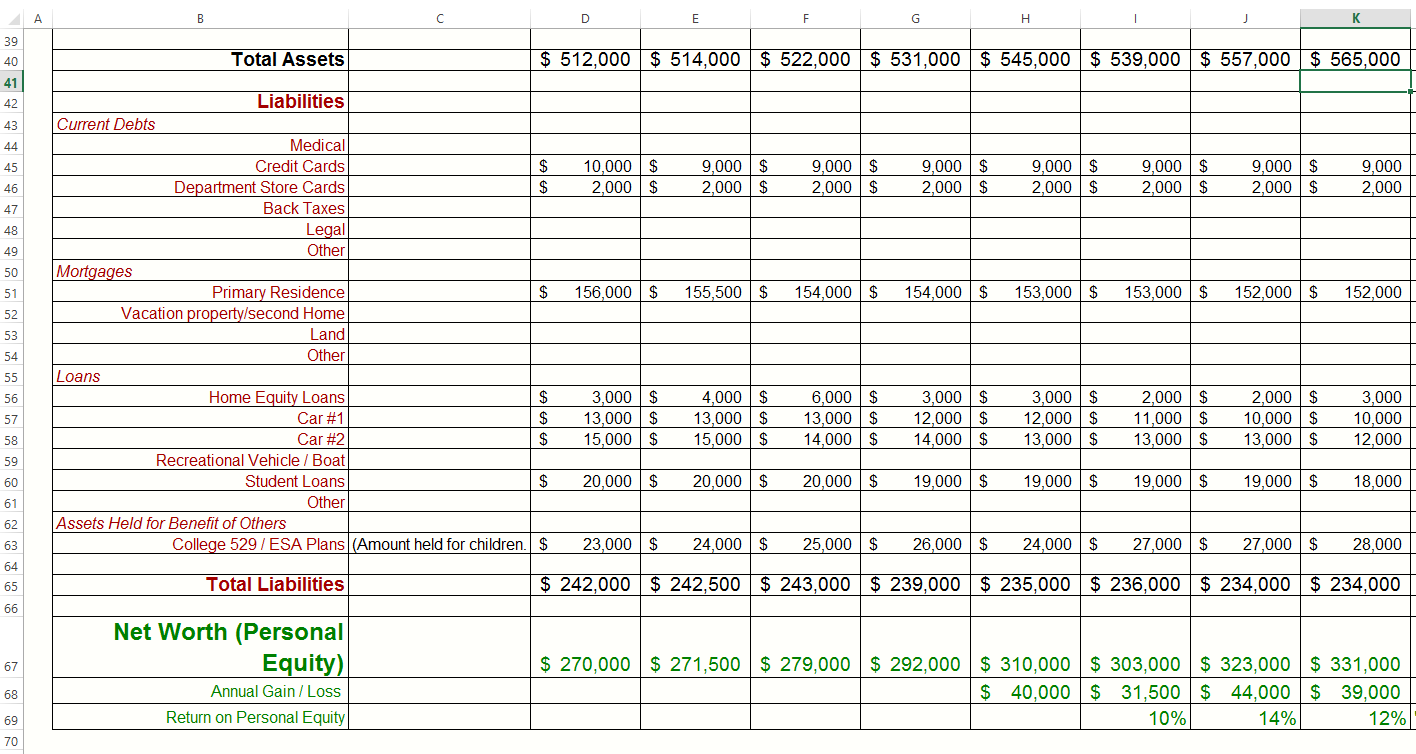

The historic average Return on Equity (ROE) of the Dow Jones Industrials is about 11%. Can you beat that? I mean in your personal financial life. This is a statistic I recommend you follow – your Return On ‘Personal’ Equity, or ROPE. Much like a business ROE, your personal return tells you how much income is returned to you as a percentage of your equity. The ROPE measures your personal profitability by revealing how much profit you generate with the money you have invested by saving and paying down debt.

The Net Worth spreadsheet available on my Research Offers page, calculates your ROPE as you track your Net Worth. Here’s a close-up to show how the mechanics of your ROPE might look:

By the way – why aren’t you tracking your Net Worth? As an investor, you should have only one goal: To increase your Net Worth over time. Unless you regularly evaluate (Total Assets minus Total Liabilities), you will not know what financial direction you are going in.

Net Worth is essential as a personal finance tool. It’s the ultimate measure of financial health. By reviewing your finances on a regular basis you can get a good feel for your financial well-being. If your Net Worth is rising, you’re probably in good financial health. If you’re net worth is shrinking, you’ll want to take a closer look at your finances to see what’s wrong.

My goal is to increase my Net Worth over the previous quarter, which means that either my expenses for the quarter were less than my income, and/or my investments have increased in market value.

The exercise of calculating your Net Worth and ROPE is really powerful. It will help you consider every major purchase you make and every loan you take or investment you make. It will have you asking a very simple question… what am I spending my money on that is increasing my net worth or decreasing my net worth?

Again, the spreadsheet is available on the Research Offers page. Keep using the spreadsheet for years and it will help you reach your financial goals.