When low interest rates play havoc with your investment planning, it’s the only fail-proof way to reach financial goals

Source: The only fail-proof way to reach your financial goals is to save more – The Globe and Mail

Source: The only fail-proof way to reach your financial goals is to save more – The Globe and Mail

Albert Einstein , one of the greatest minds of the 20th century, forever changed the landscape of science by introducing revolutionary concepts that shook our understanding of the physical world.

Learn more about the best marihuana oil is used for anxiety in this post by HMHB.

‘Sell the house, sell the car, sell the kids.’ That’s exactly how I feel – sell everything. Nothing here looks good,” Jeff Gundlach said in a July 29th interview. “The stock markets should be down massively but investors seem to have been hypnotized that nothing can go wrong.”

Gundlach, who oversees more than $100 billion at Los Angeles-based DoubleLine, said the firm went “maximum negative” on Treasuries on July 6 when the yield on the benchmark 10-year Treasury note hit 1.32 percent.

“The yield on the 10-year yield may reverse and go lower again but I am not interested. You don’t make any money. The risk-reward is horrific,” Gundlach said. “There is no upside” in Treasury prices.

Gundlach reiterated that gold and gold miners are the best alternative to Treasuries and predicted gold prices will reach $1,400. U.S. gold on Friday settled up at $1,349 per ounce.

Gundlach lambasted Federal Reserve officials yet again for talking up rate hikes for this year while the latest GDP data showed disappointing economic growth. “The Fed is out to lunch. Does the Fed look at what’s going on in the economy? It is unbelievable,” he said.

Overall, Gundlach said the Bank of Japan’s decision on Friday to stick with its minus 0.1 percent benchmark rate – and refrain from deeper cuts – reflects the limitations of monetary policy. “You can’t save your economy by destroying your financial system,” he said.

Source: ‘Sell everything,’ DoubleLine’s Gundlach says | Reuters

Since hidden role games are not all made the same, we’ve created a field guide so that you can pair the most appropriate game with your group.

Source: A Field Guide to Hidden Role Games for Any Occasion | Geek and Sundry

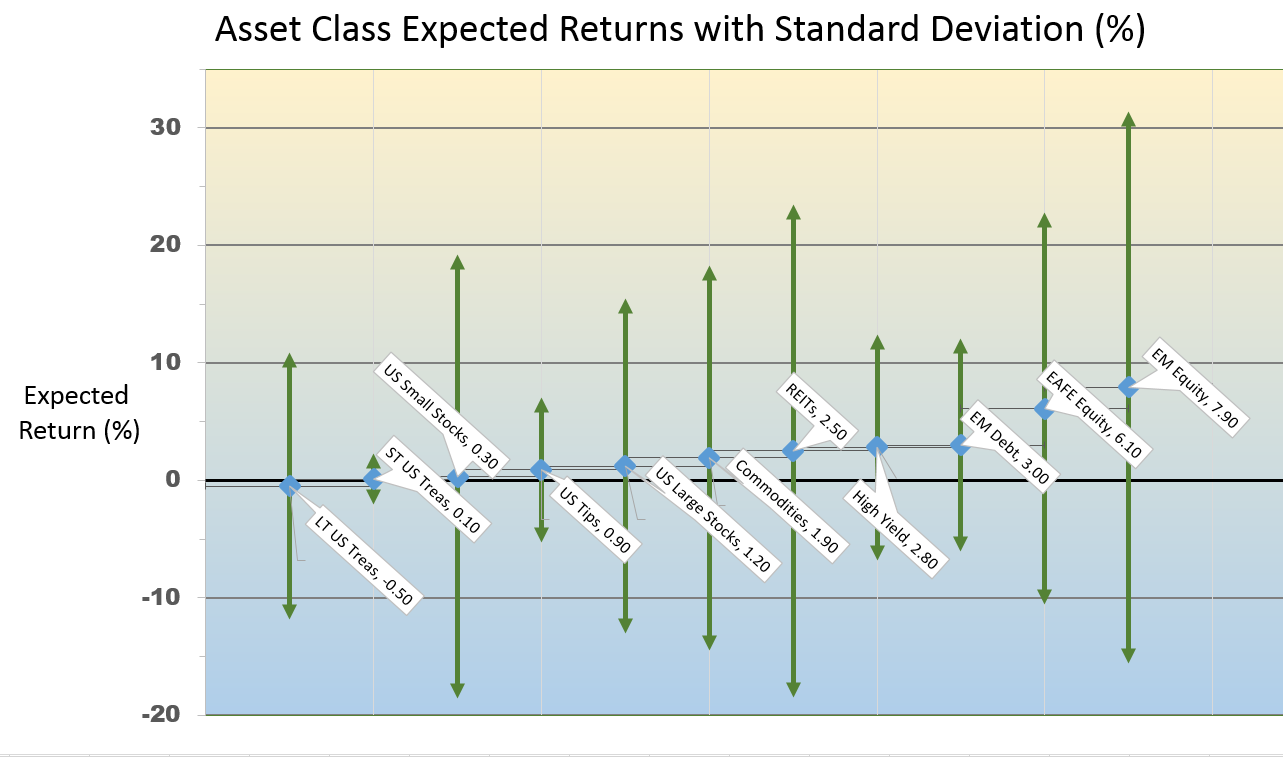

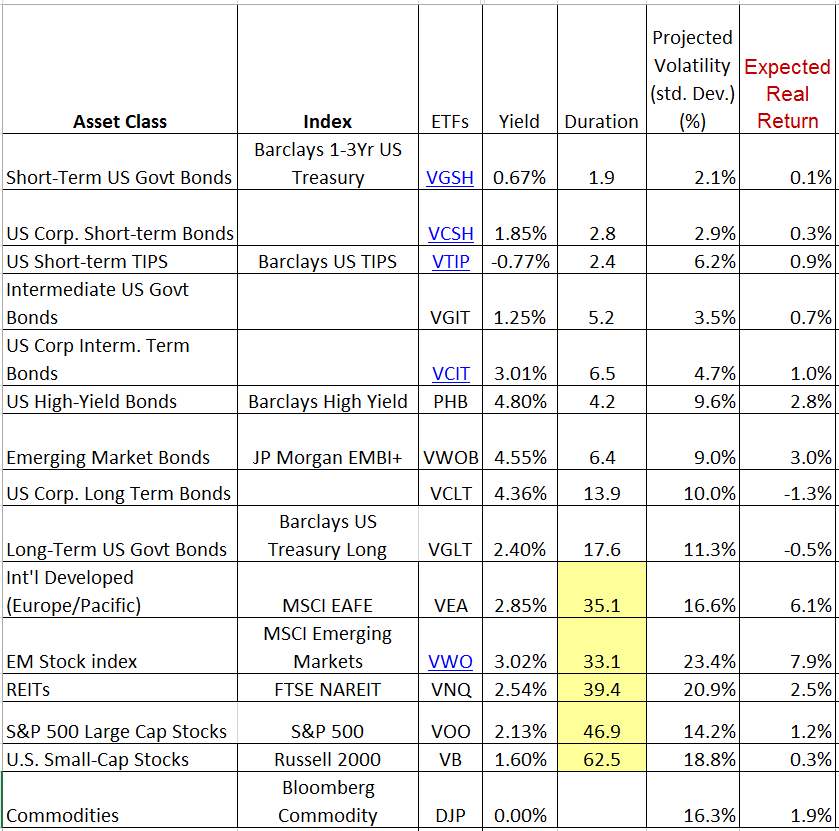

Below is a brief look at major asset classes, their forecasted annual return, price volatility, and an application of the Kelly Formula to the Asset Allocation decision. All returns are presented in real terms (net of inflation), in order to show change in investors’ actual capacity to consume.

As of 4/30/16. Source: These expected returns are calculated by Research Affiliates, LLC.

Projected future returns across most major asset classes have been compressed to near the zero bound. Their volatilities lead to near 50% or greater odds of negative returns for many assets. This is not a normal state of affairs. During normal times, US Equities will often offer 10% or greater expected returns. Only Emerging Markets come close to offering a decent investment return.

Below are these expected returns in table format, arranged in relative order of risk. My risk measure is a combination of price volatility and duration.

For stock market investing, the Kelly Formula is:

f = (u – r)/s^2

where f is the Kelly fraction, u is the expected return of the risky asset, r is the opportunity cost, and s is the standard deviation (volatility). Below I take these expected returns and apply them to the Kelly Formula (which gives the optimal bet size). The Kelly Formula, however, assumes we can adjust our allocation instantaneously – and with no trading costs. Obviously we cannot trade so often (I adjust allocations twice a year), thus this version of the formula offers no downside protection. In order to protect against short-term downside moves, in the table below I reduce the projected return by the expected value of a short-term loss. This is taken from the amount of negative volatility (seen in chart above).

The opportunity cost ‘r’ in the Kelly equation is the expected return of the next available safer investment.

Plugging these values into the Kelly Formula leads to an interesting dilemma. There is no major asset class which currently offers sufficient risk-adjusted return. Lest you think this is a normal state of affairs, here is a more ‘normal’ situation for the S&P 500:

![]()

![]()

When the S&P 500 is offering more respectable long-term returns of 11%, this version of the Kelly Formula would allocate 80% of your portfolio to the index.

The conclusion is thus: Currently it is unfortunately best to hold cash until the markets offer us something worth investing in. If you have access to a Stable Value fund, perhaps in a 401(k) plan, many are currently offering a guaranteed 1.5 – 2% return. We’ll revisit the markets in October to see where the world stands.

I’m certainly not the only one suggesting abysmal long-term returns for major asset classes. Fund manager and economist John Hussman is currently suggesting:

We currently estimate that the total return on a conventional portfolio mix of stocks, bonds and Treasury-bills is likely to average scarcely 1.5% annually over the coming decade…..At present, years of relentless quantitative easing by the Federal Reserve have driven equity valuations to the point where prospective 10-12 year S&P 500 total returns are just 0-2% by our estimates, while Treasury yields are also below 2% and Treasury bill yields are only a fraction of a percent. The combination brings the expected return on this portfolio mix to the lowest level in history outside of the valuation extremes of 1929, 1937, and 2000. Yet, because investors and policy-makers seem incapable of distinguishing realized past returns from expected future returns, they fail to see the danger in this situation.

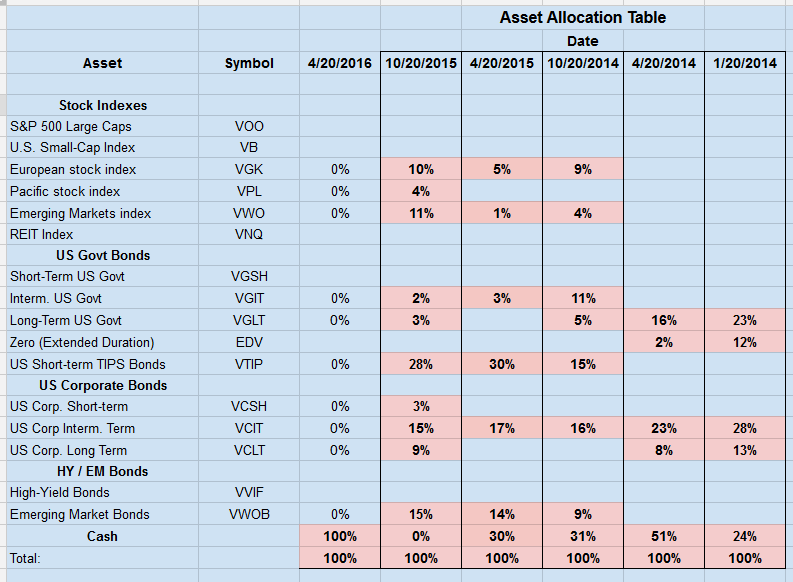

A history of changes to the Asset Allocation model is shown in Table below and may also be found on the Portfolio page.

One study suggests that more than 91.5% of a portfolio’s return is attributable to its mix of asset classes. Individual stock selection and market timing accounted for less than 7% of a diversified portfolio’s return. William Bernstein says in his book The Four Pillars of Investing, that: “The ability to estimate the long-term future returns of the major asset classes is perhaps the most important investment skill that an individual can possess.”

As people move up the income ladder, they escape material shortages and consume more. They have “things” — goods, houses, and, most importantly, education — to show for their higher earnings, but they do not have healthy finances. Having those “things” is of course an improvement over not having them, but only for the very, very rich (or the very, very unusual) is there any real escape from the pressure-cooker of American household finances.

Why can’t people live below their means, save up some money, and kick up their feet? The place to start is by looking at what they are spending their money — and particularly their loans — on. The biggest expenditure? Housing, by far. (Transportation is next, but a good portion of that — gas — is in some ways a housing cost as well, since it’s a function of one’s commute.) And the biggest sources of debt? Housing and education. The average loan burdens for mortgages and student loans dwarf auto loans or credit-card debt, the other major types of debt that Americans tend to carry.

Housing and education appear to be two distinct categories of spending, but for many families they are one and the same: For the most part, where a family lives determines where their kids go to school, and, as a result, where schools are better, houses are more costly. This is both cause and effect: Where houses are expensive, the tax base is bigger and schools have better resources, and where schools are better, there is more demand for housing. Zoning restrictions exacerbate this dynamic, because many rich municipalities with excellent public schools oppose the density that would allow more people to access their schools, which in turn drives housing prices up further. So in a sense, for many people, housing debt is education debt.

It’s all too clear why parents will spend down their last dollar (and their last borrowed dollar) on their kids’ education: In a society with dramatic income inequality and dramatic educational inequality, the cost of missing out on the best society has to offer (or, really, at the individual scale, the best any person can afford) is unfathomable. So parents spend at the brink of what they can afford.

Source: Americans facing poverty with no name – Business Insider

Source: Don Draper’s Apartment

Constant improvement is not easy. Whether it is a skill, or a positive quality, or a way of life you are looking to cultivate, staying on the positive side of the growth curve takes work.

It all comes down to self-awareness.

1. What Is My Unique Ability?

2. Am I Still Growing?

3. Am I Taking Care of Myself?

4. What Is the Next Skill I Need?

5. What Am I Most Proud of?

Source: 5 Questions Everyone Should Ask Themselves Daily to Achieve Success | Inc.com

What’s more, these are the same muscles you rely on to run, jump high, and explode upward, fighting gravity.

Source: How a Top-Flight Trainer Discovered the Most Important Exercise Every Athlete Should Do

Athletes in most sports are not concerned with raw strength or in hypertrophy (ie. “looks”). Rather it is the production of power that is of utmost importance. Few programs directly address this need. The science behind coach Flaherty’s ‘Force Number’ is very similar to my own ‘R.I.P. – Records in Power’ Training Program, which uses the formula: Power = [(Load)*(Load/Body Wt.)*(# Reps)] / (minutes). Rather than pure strength or hypertrophy (ie. ‘looks’), the R.I.P. program is designed to be optimal for training of athletic power production.

Learn More: R.I.P. Records In Power Weightlifting Program.