Herbalife (NYSE: HLF) stock today made a round trip into my “Buy zone”, then took off and gave a 25% one-day return. Herbalife, a nutritional company that uses multi-level marketing tactics, has been pressured recently by Bill Ackman of the Pershing Square hedge fund. Ackman, who has been publicly battling HLF for a year, owns a large short position in HLF. News that Ackman would give a detailed presentation Tuesday presenting his short case had brought the stock price down as low as $54 per share on Monday. When Tuesday’s presentation had little new information from Ackman, HLF stock skyrocketed more than 25%.

Here’s a look at the past 3 months of trading in HLF:

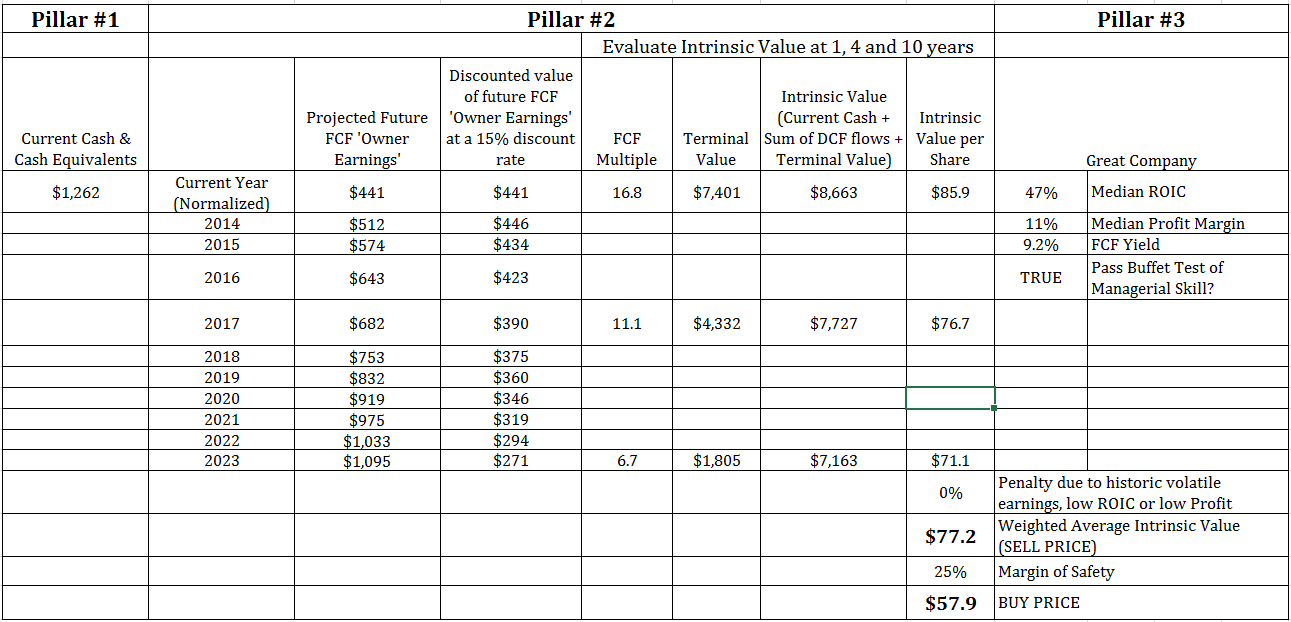

The price action in HLF has been so swift this past week that I missed the opportunity, but HLF presents a case study in my stock investing methodology. I calculate the current Intrinsic Value of HLF at $77.20. With a 25% Margin of Safety, my ‘Buy Price’ is $57.90. HLF has been on my stock watch list for a few months, where I patiently wait for stocks to fall below the Buy Price. HLF fell to as low as $54 per share Tuesday morning, offering me a chance to pick it up well below $57.90. I certainly wish I had, because the stock bounced back mightily more than 25% in one day. It is still below my Intrinsic Value, but I buy with a minimum 25% safety net. So HLF is safely back on my ‘watch’ list.

Warren Buffet has described a ‘3 Pillars Approach’ to calculating the intrinsic value of Berkshire Hathaway in several of his annual shareholder letters. The following quotes are from his 2010 Berkshire Hathaway letter:

“Though Berkshire’s intrinsic value cannot be precisely calculated, two of its three key pillars can be measured. Charlie and I rely heavily on these measurements when we make our own estimates of Berkshire’s value.”

Pillar #1:

“The first component of value is our investments: stocks, bonds and cash equivalents. At year end these totaled $158 billion at market value.”

Pillar #2:

“Berkshire’s second component of value is earnings that come from sources other than investments and insurance underwriting. These earnings are delivered by our 68 non-insurance businesses.”

Pillar #3:

“There is a third, more subjective, element to an intrinsic value calculation that can be either positive or negative: the efficacy with which retained earnings will be deployed in the future. We, as well as many other businesses, are likely to retain earnings over the next decade that will equal, or even exceed, the capital we presently employ. Some businesses will turn these retained dollars into fifty-cent pieces, others into two-dollar bills.”

The table below presents a summary of my valuation of Herbalife using the ‘3 Pillars’ Approach of Buffet. This is a version of a Discounted Cash Flow (DCF) model.

Hopefully most of the table is self-explanatory to value investors. Current year earnings are normalized, and projected into the future using conservative historic growth rates. The FCF multiple for terminal value is determined with the Stable Growth Rate equation.

NOTE: I have not done enough due diligence into Herbalife to recommend the stock. There is a lot of controversy surrounding their business practices. This trade happened quickly. If Herbalife fell into my ‘Buy zone’ again I would perform additional research prior to purchasing.

I maintain my Stock Watch list on the Portfolio page. Feel free to follow along or critique. Usually a falling stock will give me ample opportunity to buy at an attractive price. No such luck today.

[…] price has again fallen back into my ‘buy zone’ which I described in the prior article ‘Herbalife Valuation using Buffet’s ‘3 Pillars’ Approach Yields 25% One-day …‘ In that article I mentioned my calculated Intrinsic Value for HLF was $77.20. At a current […]